Government policy isn’t what makes wages rise.

Last week, Rep. Ro Khanna tweeted about the disparity in CEO and worker wage growth since 2009.

He wrote, “From 2009-2019: CEO compensation rose 105%. The minimum wage rose 0%. CEOs work hard, to be sure, but workers also deserve to be compensated for their productivity. We need to raise the wage.”

There is widespread belief in the claims that Rep. Khanna makes in this tweet. According to a 2016 survey by Stanford University, about three-fourths of Americans believe that “CEOs are not paid the correct amount relative to the average worker.” And, according to Pew Research, two-thirds of Americans support a $15 minimum wage. So, his assertions deserve a closer look.

The Myth of Wage Stagnation

First and foremost, Rep. Khanna is arguing that wages for the average American have stagnated over time — a claim that has become ubiquitous in today’s political conversation, with both those on the left and the populist right using that talking point as a cornerstone of their messaging.

The claim is not actually accurate.

The first trap Rep. Khanna falls into is conflating the lack of a government-mandated minimum wage increase with a lack of actual wage increases. In truth, wages can rise — and have — even if the federally mandated minimum wage does not.

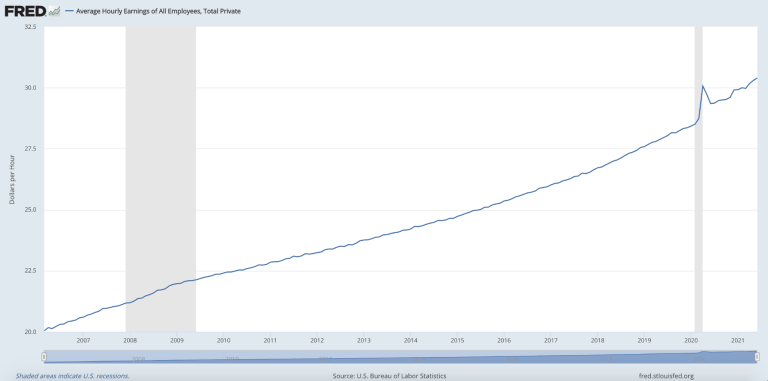

According to Federal Reserve Economic Data (FRED), average hourly earnings have increased from $21.97 in January of 2009 to $30.40 in June of 2021. That represents a 38% increase.

And income has actually risen even more than that due to non-wage compensation taking up a larger portion of total compensation over time. The New York Times reported that non-wage compensation accounted for 32 percent of total earnings in 2018, up from 27 percent in 2000. Non-wage compensation includes “bonuses, paid leave and company contributions to insurance and retirement plans.”

The Main Reason Wages Rise

Even though the federal government has not increased its minimum wage over the past decade or so, wages still rose due to the interplay between investment and competition.

When a company makes a profit — meaning their total revenue exceeds their total costs — they have capital available to them beyond what is needed to cover their current total costs. As a result, they will usually invest some percentage of that additional capital back into their business in order to improve productive capacity and create the possibility of even greater profit in the future. This investment can come in many forms, including training existing workers in more advanced skills or integrating new technology and tools into the business.

By investing in new technology or skills, companies can increase each worker’s productivity. This means each worker has the ability to generate more additional revenue for the firm than they could before, creating upward pressure on wages.

As a demonstration, take the following scenario: Company A was paying an employee, who was generating $16 per hour of additional revenue, $14 per hour — therefore making $2 of profit. Then, after the company invested in new technology and training, that employee began to generate $19 per hour of additional revenue for the company — increasing the firm’s profit to $5 per hour.

It may seem that the worker is being taken advantage of because they are now generating more revenue for the company while not receiving a corresponding increase in pay. But the competition of a free market system solves this.

Company A may well increase that employee’s pay. But, if they do not, Company B now has the opportunity to outbid Company A for the worker’s labor. If they offer a higher wage — say $16 per hour — in order to lure the worker away from Company A, they will still be making a profit. And the only way for Company A to retain the employee would be to offer even more than that.

To recap: the investment of Company A increased the productivity of the worker, thus creating competition between multiple firms for their labor and, in the end, raising their wage.

In the recent past, such competition for labor has led to wage increases for hundreds of thousands of workers at places ranging from Walmart to Costco to Amazon. And, because businesses are currently trying to attract as many workers as possible amid our labor shortage, we see many firms raising wages and offering other benefits as well.

“There is no other method,” as the great economist Ludwig von Mises summed it up, “to make wage rates rise than by investing more capital per worker. More investment of capital means: to give to the laborer more efficient tools. With the aid of better tools and machines, the quantity of the products increases and their quality improves. As the employer consequently will be in a position to obtain from the consumers more for what the employee has produced in one hour of work, he is able—and, by the competition of other employers, forced—to pay a higher price for the man’s work.”

The Consequences of a Minimum Wage Hike

At the end of Rep. Khanna’s tweet, he calls on Congress to “raise the wage.” But raising the minimum wage to $15 per hour would actually hurt the very people Rep. Khanna is intending to help — namely low-skilled workers in general and teenagers in particular.

A minimum wage is simply a floor on the price of labor, meaning employers are unable (by law) to pay below that. If a minimum wage was set at $15 per hour, that means all people who cannot produce more than $15 of additional revenue per hour will not be hired — and thus will be making no money at all. After all, if a company paid someone $15 per hour who only has a productivity of $12 per hour, the business would actually be losing money and, if they kept at it for long enough, would ultimately go out of business.

Thus the minimum wage especially harms the young, the inexperienced, the disabled, and individuals struggling in life, because they tend to be at the bottom of the value-creation ladder. And what is especially pernicious about the minimum wage, is that it prevents such individuals from ever being able to climb the value-creation/earnings ladder, because it knocks out its bottom rungs.

The minimum wage is a poverty trap. And, hiking the minimum wage to $15/hour (almost doubling it) would just make that poverty trap even bigger, economically bogging down even more marginal would-be workers.

And this has not just been reasoned-out theoretically, but actually demonstrated empirically. A recent paper surveying the economic literature on minimum wage hikes came to the conclusion that “there is a clear preponderance” of evidence that they result in negative outcomes, most clearly “for teens and young adults as well as the less-educated.”

Intentions ≠ Consequences

We all, of course, have a shared goal of higher wages and greater prosperity for all Americans — not just those on the top of the economic ladder. But well-meaning people in government rarely achieve their intended goals when their primary aim is just to “do something” about a given problem (in this case, the perceived stagnation of wages). Government schemes often only serve to make problems worse than they need to be, as is the case when it comes to minimum wage laws.

Famed free-market economist Thomas Sowell wrote in his best-selling book, Basic Economics: A Common Sense Guide to the Economy, “nothing is easier than to have good intentions but, without an understanding of how an economy works, good intentions can lead to disastrous consequences for a whole nation.”

This is exactly right.

So while the good-hearted advocates for an increased minimum wage truly believe that their policy will redound to the benefit of the average worker, their misunderstanding of how the economy works will inevitably lead to, in Sowell’s words, “disastrous consequences for a whole nation” in the form of unemployment.