Government control in the name of sovereignty.

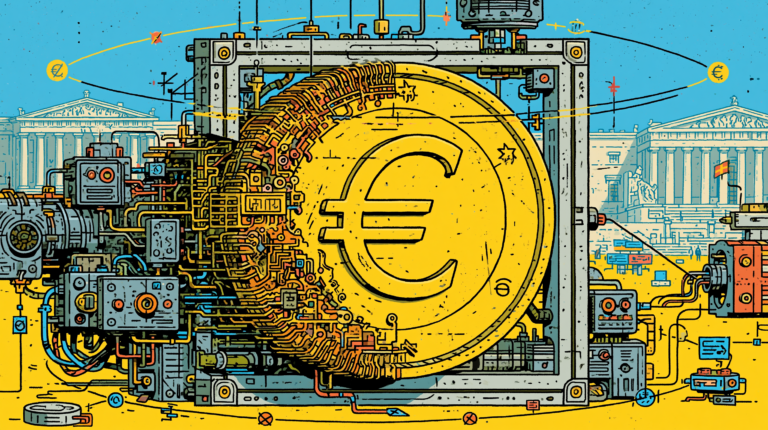

For years, the digital euro was presented by the European Central Bank (ECB) merely as a modern and practical alternative to banknotes and coins. It has now been openly acknowledged that the project is intended to respond to the dominance of American payment companies. Visa and Mastercard process 61% of card payments in the euro area, according to the ECB’s own data, and it is this dependence that Brussels intends to break.

On June 23, the European Parliament’s Committee on Economic and Monetary Affairs (ECON) approved its negotiating position on the digital euro legislative package by 43 votes to 14. Although this approval does not constitute the final law, a final agreement with the Council is expected by the end of 2026, with implementation projected to begin only from 2029 onward.

The project, which has historically been justified by the ECB as merely a matter of convenience compared with cash, was this time presented in a European Parliament statement as a genuinely European payment option, in an attempt to counter the dominance of major American payment companies, in what could represent yet another escalation of tensions in transatlantic relations. Visa and Mastercard’s dominance of cross-border transactions in Europe generates billions of euros in fees; a significant reduction in that dominance would weaken the dollar, represent an economic loss for these American companies, and threaten one of Washington’s soft-power tools. Whatever the outcome of this dispute between blocs, it is the European citizen who first bears the cost of the response chosen by Brussels.

This development reflects the increasingly protectionist approach that the European Union has adopted in the technological sphere, as seen with the Digital Markets Act and the recent Tech Sovereignty Package, making open competition and private innovation more difficult. Under the pretext of defending European sovereignty, Brussels has chosen to create centralized public infrastructures. But money is not infrastructure. It is the instrument through which the state and the citizen negotiate, every day, the boundaries of individual freedom. That is why, since the beginning of discussions on the digital euro, a particularly dangerous direction of travel has been emerging.

According to the negotiating position that has now been approved, it will not be citizens, but rather the European Commission, acting on a recommendation from the ECB, that will determine the maximum amount of digital euros each person may hold, likely around €3,000 (just under $3,500) with periodic reviews.

In addition, companies will not be allowed to maintain digital euro balances for more than 24 hours, except for accumulating received payments, which must be automatically transferred after that period.

This prevents businesses from using the digital euro as a treasury management tool, a liquidity reserve, or for routine payments such as suppliers and payroll. Through this rule, Brussels strengthens centralized state control and significantly reduces the usefulness of the digital euro for the business sector. Companies lose freedom and options.

Holding limits and restrictions imposed on businesses, while shocking to advocates of freedom, are not new. These ideas have been embedded in the digital euro project since its initial stages. In the legislative proposal presented by the European Commission in 2023, the ECB and Brussels explicitly acknowledged that limits would be imposed on the amount of digital euros each citizen could hold, under the familiar justification of “protection,” in this case, protecting financial stability and preventing deposit flight from commercial banks. The novelty, therefore, does not lie in the principle but in its implementation. What was in 2023 an open possibility has now become a concrete decision, clearly made without regard for the wishes of citizens themselves.

These conditions follow the same logic of centralized control found in China’s digital currency, the digital yuan (e-CNY). In the Chinese system, there is also the possibility of obtaining higher limits in exchange for surrendering more personal data and accepting less privacy, a model of “tiered privacy” in which freedom is always sacrificed and only the degree of submission to the state remains open to choice. Thus, in order to reduce dependence on American payment companies in the name of “European sovereignty,” instead of strengthening private competition and liberalizing the market, Europe is importing the model of state control that China has refined.

Although the ECB publicly denies that the digital euro will be a programmable currency, these kinds of technological and centralized solutions always leave open the possibility that conditional functionalities may be built upon their architecture. Money can be made to expire, be conditioned, or be tracked, transforming it into a public-policy instrument far more powerful than cash has ever been. To combat an alleged external dependence on North America, Europe is creating an even more dangerous internal dependence, one in which money ceases to be an instrument of individual freedom and open markets, and instead becomes a tool of control and geopolitical rivalry.

In the end, the digital euro does not liberate Europe, modernize it, or make payments more convenient. It merely changes who holds control, shifting it from American private companies to European public authorities, and strengthens that control in the process. At its core, this project reveals a profound civilizational choice: money ceases to belong primarily to individuals, as the state assumes the power to define the limits of financial freedom.

Brussels not only threatens the freedom of its citizens, but also risks escalating transatlantic tensions. A direct challenge to the dominance of US payment giants and the dollar’s global infrastructure is unlikely to be ignored passively in Washington. The more money is transformed into an instrument of public policy and geopolitical rivalry, the smaller the space becomes for individual freedom and open markets.