The US economy is on the edge of a huge correction.

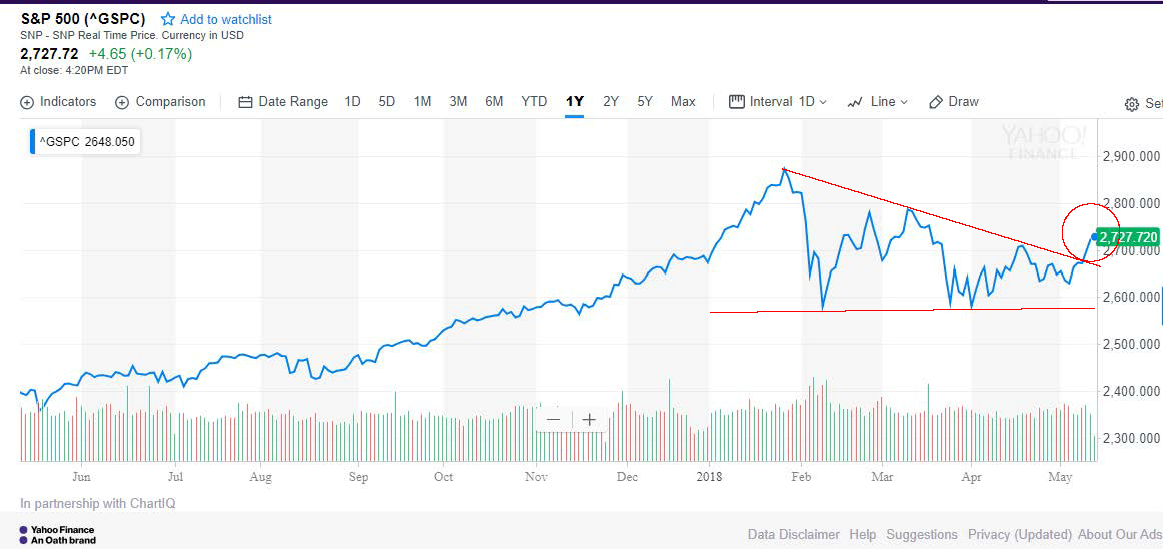

U.S. stock markets remain volatile and their direction uncertain, although the S&P 500 may have broken out of what technical traders would call a “bullish triangle,” which began forming after the market fell approximately 12 percent in early February from a high of 2,872 the previous month. However, traders will also tell you every technical pattern can tell at least two stories. One must look to the fundamentals for confirmation, and they have been anything but unanimous on the underlying economy.

Stagnant Growth

Corporate earnings have been strong, but that may not be a real indicator of economic growth, as much of the earnings per share increases are due to stock buybacks rather than organically increasing profits. And jobs numbers continue to disappoint. Not only did April’s number come in lower than expectations, January’s number was adjusted down by a whopping 63,000 jobs.

GDP growth slightly beat expectations at 2.3 percent but is far below the 5.4 percent predicted by the Atlanta Federal Reserve just two months ago.

Job growth for the first four months of 2018 is still ahead of 2017, but by a lot less than previously thought, and we don’t know if March and April numbers will be adjusted downward. Consumer spending remains weak, and surging energy prices, especially gasoline, may continue to eat up what would otherwise be discretionary spending dollars for average households. While unemployment is at or near record lows, so is workforce participation—a statistic conservatives seem to have completely forgotten about since President Trump was inaugurated.

GDP growth slightly beat expectations at 2.3 percent but is far below the 5.4 percent predicted by the Atlanta Federal Reserve just two months ago. Despite missing the real number by a country mile, the same institution is now predicting 4.0 percent growth for Q2. Why should anyone expect this “irrational exuberance” to be any more accurate than last quarter’s?

Tax Cuts?

The trump card (pun intended) is supposed to be tax cuts. Although they obviously haven’t delivered the jobs or growth promised to date, sooner or later the supposedly smaller slice the government is taking must result in more domestic investment, jobs, production, and growth.

The problem is taxes haven’t really been cut. They’ve simply been deferred. The federal government is going to spend more this year, and every year for the foreseeable future, than in any year in U.S. history. That spending is ultimately going to be paid with taxes, either now or in the future.

Lowering corporate and individual rates now merely allows Americans to pay for the spending at a slower rate.

Lowering corporate and individual rates now merely allows Americans to pay for the spending at a slower rate. But unless you believe in leprechauns who donate their pots of gold to the government, the $4.1 trillion the government will spend this year must come from the American economy. The roughly $1.1 trillion in spending not covered by current tax revenues will be borrowed, meaning Americans will pay for not only the spending but the interest due to lenders when the bonds come due. All that spending comes at the expense of productive investment in the private sector.

Contrary to conventional wisdom, the government borrowing money now doesn’t just harm future generations. It hurts economic growth in the present, the same year the money is borrowed. Every Treasury bond purchased on the open market represents a U.S. corporate bond that isn’t purchased. The result is new jobs that aren’t created, new production that doesn’t occur, and existing production that doesn’t expand.

Price Inflation

The bill is also paid for partially in price inflation, which the government tells us is low. But that is just another deceiving statistic for two reasons. First, by its own admission, the government manipulates price inflation numbers lower with “hedonic adjustments” (negating price increases because a product has new features), “substitution” (ignoring price increases under the assumption consumers will just buy something else), and other accounting tricks.

Second, and rarely mentioned, is the massive price deflation we should be seeing. Technology is allowing the economy to produce more with less people. With U.S. manufacturing output at or near all-time highs while using only a fraction of the personnel it once required, for example, the prices of manufactured goods should be falling, just as they did throughout the 19th century. The natural result of economic growth is falling prices. If you increase supply, all other things being equal, prices will fall.

The key vote in Congress over the past year wasn’t to cut tax rates; it was to increase federal spending.

The massive wave of baby-boomer retirements is also a deflationary force. Retirees spend about 37 percent less on average than working adults. That decreased demand while supply is increasing should result in sharply falling prices. That prices can rise 1-2 percent (or higher, if measured honestly) under present conditions is a testament to the magnitude of the Federal Reserve’s inflationary interventions, especially over the past decade.

The privilege of printing the world’s currency has allowed the United States to direct massive amounts of capital towards non-productive endeavors, including avoidable wars that have yielded no discernible benefit to the taxpayers who fund them, a freakishly oversized military establishment even in peacetime, health care and higher-education industries that cannot survive as they are without massive subsidies for the former and government-backed loans for the latter, an entire generation owed entitlement benefits future workers can’t possibly underwrite, and a $21 trillion federal debt the government can’t possibly pay back.

Those economic distortions represent a mega-bubble that will pop, just as all the others have, but the results will be far more catastrophic due to the relative size of the problems. With the federal funds rate target still below 2 percent and the signs of a correction already appearing, we may be at the leading edge of the worst correction in U.S. history. Even if the Fed has one more trick up its sleeve, that must certainly be its last.

The key vote in Congress over the past year wasn’t to cut tax rates; it was to increase federal spending. We’re not seeing the jobs and growth expected because the federal government is consuming more of what society produces rather than less. Until that trend reverses and the fundamental, structural problems with the U.S. economy are addressed, real economic growth will continue to prove elusive.