Let’s buckle up and see what 2019 brings to the table.

The debt crisis in the Eurozone is getting no better, even in the wake of the new year. The five countries in the Eurozone with the highest debt-to-GDP ratio in the third quarter of 2018 were Greece, Italy, Portugal, Belgium, and Spain. The total debt of Greece is around 182.2 percent of its GDP and that of Italy is 133 percent, according to Statista. Although giant economies like the US and Japan have been running huge debts for years, it is yet to be seen what waits on the other end of the tunnel.

The recent Italian political agenda to raise its budget deficit to 2.4 percent for the next three years was given a thumbs down by the EU. A country that is already creeping with huge debts trying to raise funds by increasing deficits is similar to sleepwalking into a busy highway. Dawdling economic growth coupled with low-yield investment options are dragging these indebted economies toward insolvency and perhaps another global recession.

General Government Debt as a Percentage of GDP in Eurozone

Many people think that the whole idea of this massive debt financing is the crux of Keynesian economics. Indeed, Keynes proposed government spending through deficit financing at times of recession and depression. The idea was that the autonomous investment made by the government would generate more employment opportunities and would convalesce the shattered business confidence among the investors. This was thought to give a boost to economic activity, which would help troubled economies gradually recover from depression.

The Keynesian model was tested during the Great Depression when massive deficit spending was employed to counteract the economic contraction. Though the Keynesian experiment was not exactly a success (the depression lasted 10 years), a narrative developed that this deficit spending “saved capitalism from itself.” Ever since, many economists have favored deficit financing to boost economic activity.

In any event, Keynes never advocated full-time deficit financing. He proposed that governments should create enough surplus in times of prosperity that can be used during times of distress. This idea was comfortably ignored by developed economies, including the US, which have resorted to continuous deficit financing to boost economic growth. These economies, however, cannot escape the massive debt trap by simply writing them off.

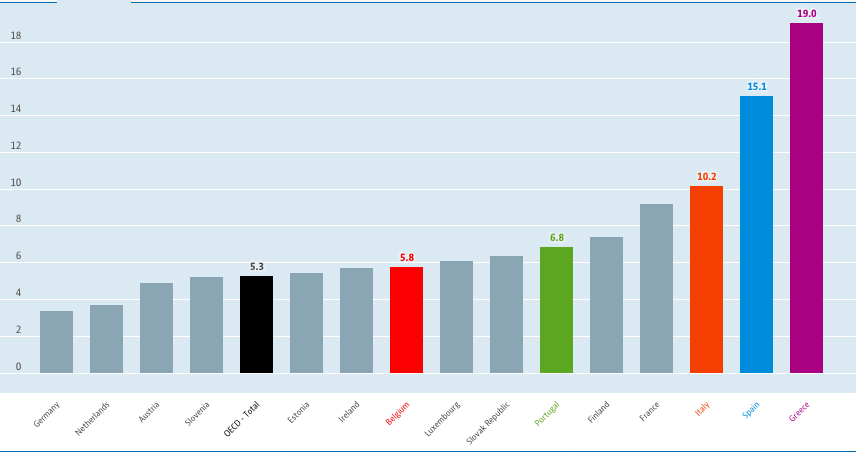

Despite the recurrent monetary assistance and policy support, job creation is weak.

Delving deeper into the macroeconomic aspects of deficit financing, any additional investment in the economy is expected to generate employment opportunities and thereby provide income to people, which would ultimately be reflected in the GDP of the country. A government is supposed to keep an eye on its budget deficits, and as the economy prospers with ample investments and increased employment opportunities, it is required to cut down those deficits subsequently.

The question now is whether the massive quantity of bailouts these countries have instituted paved the path to long-term prosperity. A close look at key statistics suggests they have not. Unemployment rates, for example, are still very high in most of these highly indebted European economies. Despite the recurrent monetary assistance and policy support, job creation is weak, which might imply that the debt financing is channelized in a nonproductive direction. Belgium and Portugal have performed relatively better than the other highly indebted countries in the list in combating unemployment.

Unemployment Rate (Total, % of labor force, Q4 2018)

Without curbing the high levels of unemployment, these economies cannot ensure a healthy pace of economic growth. As per the OECD reports, the unemployment rates in Spain and Italy in the last quarter of 2018 were 19 percent and 10.2 percent respectively. Although it can be argued that over the years the unemployment rates have come down, with the public debts soaring they need to frame a solid plan for recovery.

There is more to be added to the 2019 chapter of the European debt crisis. With the Brexit plan almost finalized, the common EU funds will dwindle, as the UK was one of the significant contributors to the common budget. This is expected to make the crisis worse. Let’s buckle up and see what 2019 brings to the table.