The history of a destructive fallacy

In most circumstances, when a model breaks down and ceases to provide valuable information, it gets tossed out the window. Not so with the Phillips Curve, which still informs the way today’s central bankers think about the relationship between unemployment and inflation.

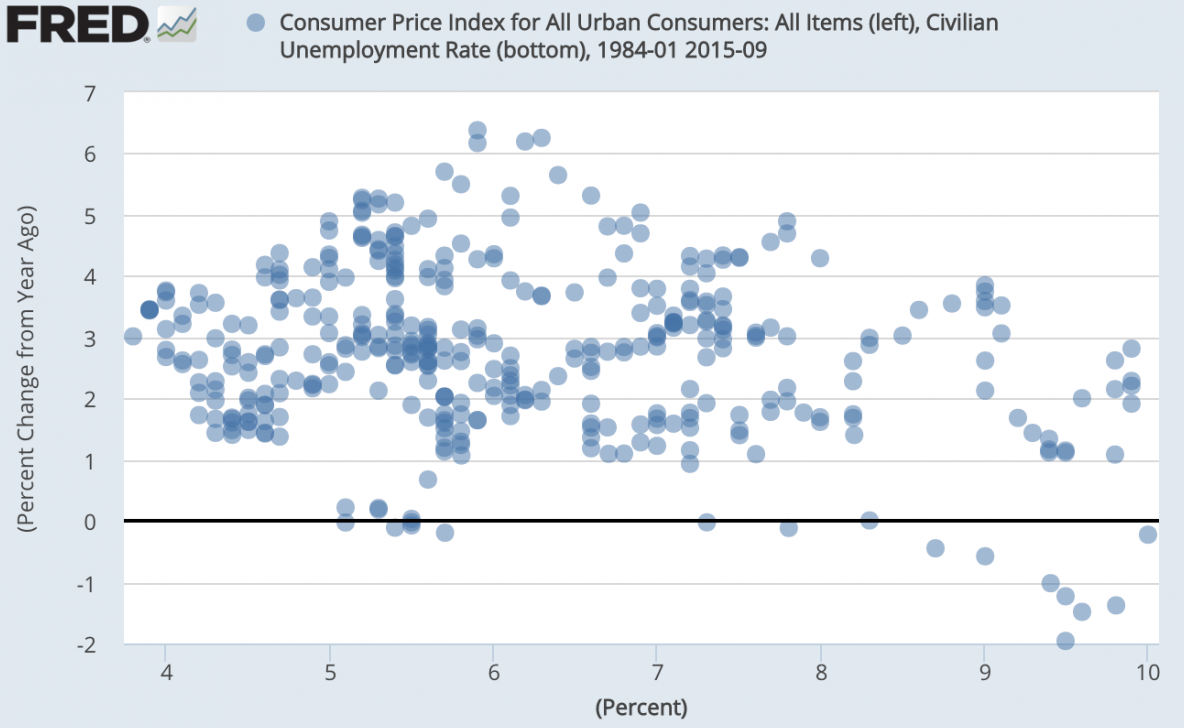

The unemployment rate has fallen from a peak of 10 percent in October 2009 to 5.1 percent in September. Yet wage growth has been flat-lining at 2 percent, year over year, while inflation remains non-existent, undershooting the Federal Reserve’s 2 percent target for the last 3 1/2 years.

Alas, hope springs eternal.

“Some tentative hints of a pickup in the pace of wage gains may indicate that the objective of full employment is coming closer into view,” Fed chief Janet Yellen said in July.

Closer, perhaps, but still over the horizon.

Yellen is perhaps the Fed official most closely associated with the Phillips Curve, the idea that there exists a trade-off between unemployment and inflation. Some history is in order.

The Phillips Curve originated with New Zealand economist A.W. Phillips, who plotted U.K. data on unemployment and wages from 1861 to 1957 and observed a consistent inverse relationship between the two. He published his findings in 1958.

“It was an ex-post relationship observed by Bill Phillips,” said Michael Bordo, an economic historian at Rutgers University. “He didn’t talk much about a trade-off.”

That was left to those who followed. In 1960, Canadian economist Richard Lipsey provided the theoretical justification for the Phillips Curve based on the idea that wages adjust to an excess demand for labor. In the same year, Paul Samuelson and Robert Solow looked at the U.S. data and found periods when wage and unemployment rates moved inversely, as they did in the U.K., along with some gaping inconsistencies (1933-1941), which they explained in terms of New Deal policies.

The Samuelson and Solow paper was the first to suggest a possible role for government policy in influencing the perceived trade-off, with inflation now substituting for wages. And the timing was perfect: The 1960s witnessed the rise of Keynesian economists, who were only too happy to use government policy to reduce unemployment. Pretty soon, the Phillips Curve had made its way into academia (Samuelson’s textbook, Economics) and was influencing policy makers in Washington (Economic Report of the President, 1962).

In the late 1960s, Edmund Phelps and Milton Friedman challenged the notion of any long-term trade-off between unemployment and inflation. In the long run, expansionary monetary and fiscal policies could only produce lower unemployment at the expense of permanently higher inflation because workers would realize their money wages weren’t keeping up with inflation. Try as they might, policy makers could not influence some unobservable natural rate of unemployment.

The stagflation of the 1970s — high unemployment and high inflation — proved Friedman and Phelps correct. The misery index, or the sum of the two variables, peaked at 21.8 percent in 1980. Both unemployment and inflation declined through most of the 1990s. The current decade has seen low unemployment, at least as measured by the official rate, accompanied by minimal inflation.

Still, the idea of a trade-off between unemployment and inflation — and the Fed’s role in facilitating it — persists to this day.

“I don’t recall tracking the Phillips Curve any time at an FOMC meeting,” said Al Broaddus, who was president of the Richmond Fed from 1993 to 2004. But “it’s in the woodwork, in the infrastructure.”

It’s also in the Fed’s econometric model, known as FRB/US. Former Fed chief Paul Volcker didn’t subscribe to the Phillips Curve, according to Bordo. Alan Greenspan was a skeptic. Ben Bernanke had his hands full with a potential collapse of the financial system. Any trade-off between unemployment and inflation was supplanted by the one between life and death.

Yellen is a believer, not only in the Fed’s mandate to deliver full employment in the context of stable prices but also in its ability to do so. Wages are almost always mentioned in the Fed minutes: something to the effect that the absence of wage pressure might be a sign that the natural rate of unemployment is lower than previously thought.

In the minutes from the March 17-18 meeting, a few participants dared to suggest that “wages might not be a useful yardstick” for evaluating labor market slack, citing some specific reasons — the long lags between a decline in unemployment and a pick-up in wages, for example — as to why not.

Over the years, various Fed officials have advocated a departure from the Phillips Curve to assess the stance of monetary policy. In the late 1980s, Fed Vice Chairman Manley Johnson introduced the idea of auction-market indicators — the Treasury yield curve, commodity prices and the foreign exchange value of the dollar — to a largely deaf audience.

The Phillips Curve has survived, even prospered, as a policy guide, perhaps because it has an intuitive appeal.

“As a general proposition, how can you avoid the notion that if you are pushing on the economy’s capacity, wages and prices will rise?” Solow said to me in a phone interview.

As a general proposition, you can’t. What about as an empirical relationship? Economists have looked for one but can’t seem to find it. Even a layman would be hard-pressed to find a consistent inverse relationship between unemployment and inflation — or even an inconsistent one — from this graph.

The most definitive conclusion one can draw about an empirical relationship between unemployment and inflation should serve as a warning to policy makers who rely on it: There is a relationship. We’re just not sure what it is right now.

This piece first appeared at e21, a project of the Manhattan Institute.