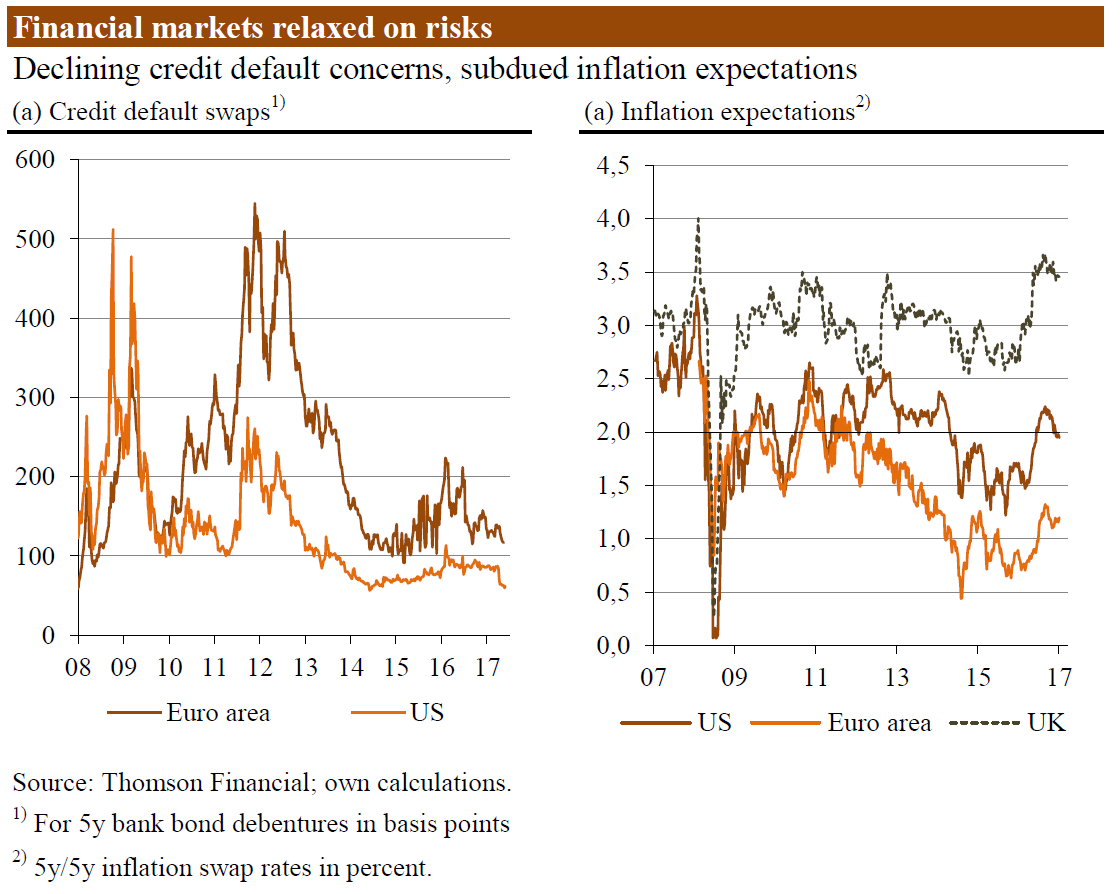

Financial markets seem to be entirely ignorant of how things will turn sour.

Economic growth has returned. Production and employment slope upwards in most countries of the Western world. However, economic recovery has been accompanied and fueled by an unprecedented expansionary monetary policy.

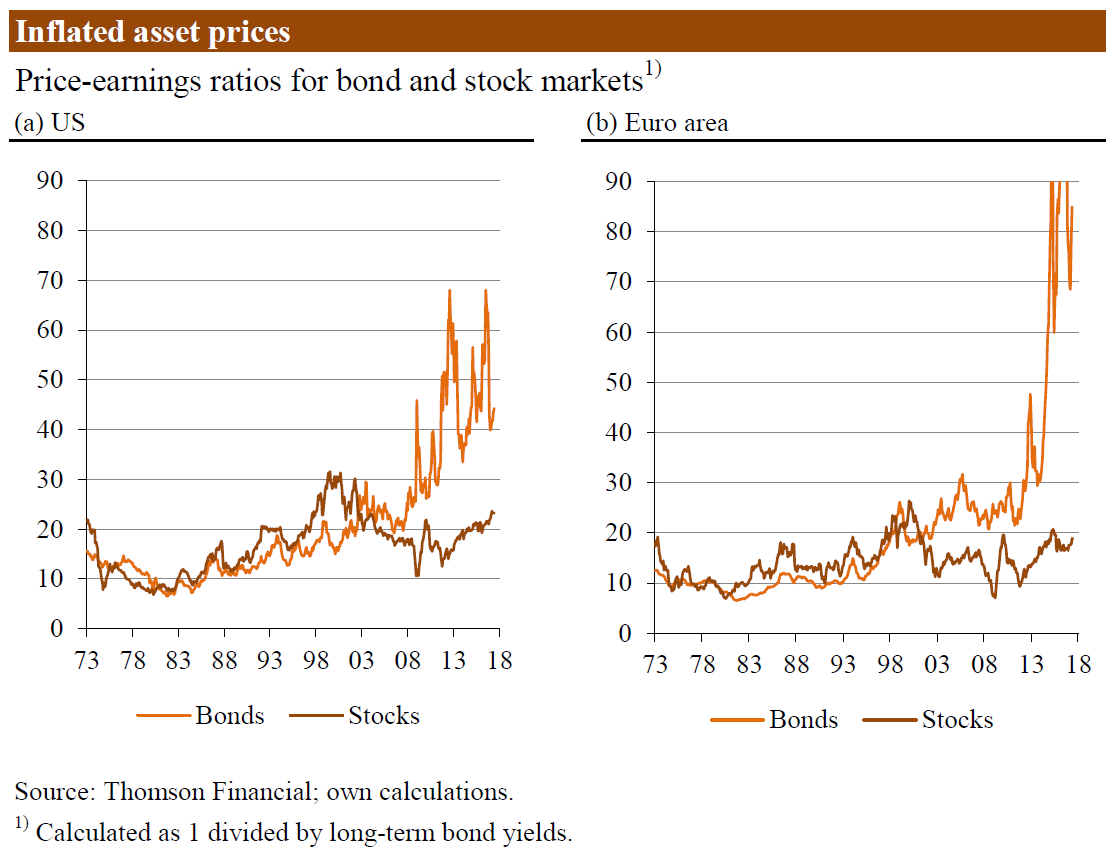

Bond prices have been inflated to an extraordinary degree.

Interest rates have been pushed down to extremely low levels, and central banks have de facto provided financial markets with a safety net: Investors can rest assured that central banks are willing and prepared to fend off another crisis – ‘whatever it takes.’

As a result, various financial asset prices have been pulled up to elevated valuation levels. In particular bond prices have been inflated to an extraordinary degree. For instance, the price-earnings-ratio for the US 10-year Treasury yield stands around 44, while the equivalent for the Eurozone trades at 85. In other words, the investor has to wait 44 years (and 85 years, respectively) to recover the bonds’ purchasing price through coupon payments.

At the same time, valuation levels of the stock markets have been edging up as well. This can in part be attributed to the extraordinarily low interest rates: Future corporate earnings are discounted by low yields, translating into higher stock prices. Furthermore, the ongoing economic recovery makes investors more confident with regards to the growth of future corporate earnings. That said, any investor should consider it important to learn more about the nature of the current recovery.

Sooner or later the monetary illusion must evaporate.

If and when central banks, in cooperation with commercial banks, increase the outstanding quantity of money through credit expansion – namely credit that is not backed up by “real savings” – an artificial upswing (“boom”) is triggered. Artificial credit expansion lowers market interest rates (to below the level that would prevail had there been no credit expansion ‘out of thin air’). Investment and consumption expenditures go up; jobs are created. But it cannot go on forever.

Sooner or later the monetary illusion must evaporate. Entrepreneurs will suddenly realize that their investment returns fall short of expectations. Sales will disappoint, and input costs turn out to be higher than originally anticipated. Firms liquidate flop investments, shedding jobs. The boom turns into a bust.

In an attempt to fend off the collapse, the central banks will rush in, lowering interest rates and pumping in new money to keep struggling borrowers afloat. The economy gets trapped in the boom-and-bust cycles.

Indeed, to keep the boom going, central banks have to keep pushing down the interest rates and make sure that new credit and money keeps flowing into the system. That said, the latest attempts by the US Federal Reserve (Fed) to bring short-term rates back up makes boom turning to bust increasingly likely. The same goes for the European Central Bank (ECB), which also signals that it might sooner or later end its overly expansionary interest rate policy.

Another bust would presumably be pretty painful for the highly leveraged economies. However, financial markets seem to be entirely ignorant of the scenario in which things turn sour.

Inflation will not only continue but ultimately accelerate.

On the one hand, investor credit default concerns have declined to relatively low levels. On the other hand, inflation expectations have remained subdued. Looking ahead, it seems to be really difficult to understand that we can have both at the same time.

Unfortunately, there is reason to expect that inflation – in the form of asset price inflation and/or consumer price inflation – will not only continue but ultimately accelerate. This is because, in times of crisis, inflation (the increase in the quantity of money) is seen as the least evil policy choice.

As Ludwig von Mises (1881 – 1973) succinctly put it :

In the opinion of the public, more inflation and more credit expansion are the only remedy against the evils which inflation and credit expansion have brought about.”