The Fed put us in this predicament. Only the market can get us out of it.

Since hitting rock bottom in 2009, stock prices have consistently increased without much volatility — that is, until these first few days of February when the Dow Jones Industrial Average fell over 2,200 points (-8.5%) and the S&P 500 tumbled 7.9% from their late-January highs. The most popular measure of stock market volatility, VIX, also spiked dramatically to levels not seen since 2011 and 2009.

- Tax reform could have caused some extra uncertainty about the future for all businesses.

- Bond markets indicate an increase in future price inflation, which means that the cost of doing business could increase.

- The increase in expected inflation coupled with a new, optimistic-looking release of official data on wages across the US might be used by the Federal Reserve to justify further interest rate hikes.

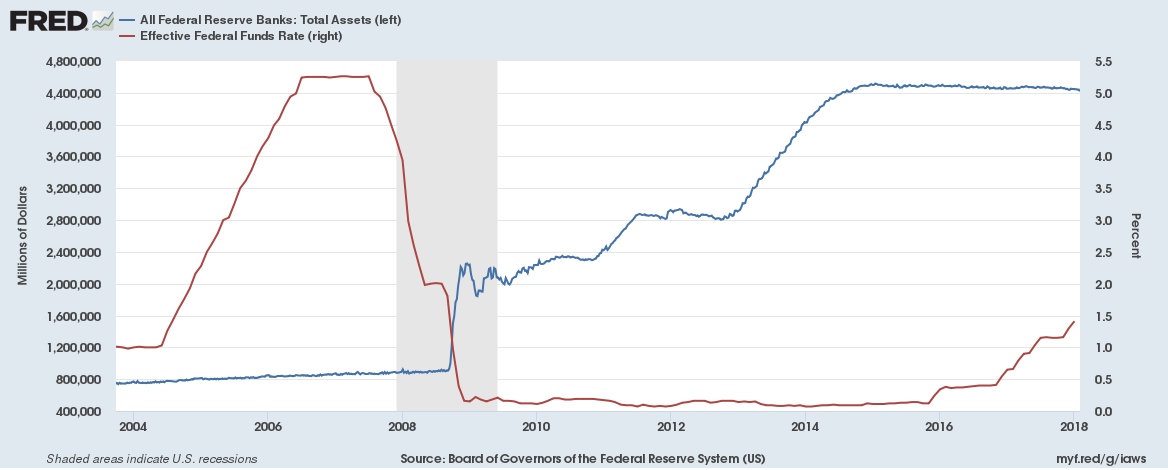

But to really get to the bottom of the current stock market decline, we need to go back to the Federal Reserve’s response to the 2007-08 crisis.

Unprecedented Monetary Policy

During that financial and economic collapse, the Federal Reserve responded in unprecedented ways. We saw the biggest expansions of credit and the lowest interbank lending rates ever.

(The blue line above shows the Federal Reserve’s balance sheet expansions. The red line is the Federal Funds Rate, or the rate banks pay each other for loans. It is viewed as the basis for all other loan rates in the US. Together, these show the unprecedented expansionary monetary policy of the Fed in response to the most recent recession.)

The Federal Reserve was pouring trillions of dollars into the financial sector and banking system and making it cheaper than ever for those firms to borrow in an attempt to stimulate more spending and employment throughout the economy. They wanted home prices and asset prices (including stocks) to stop falling and return to the seemingly irreversible positive trend they had through the mid-2000s.

But the stock market crash and the housing market bust were vital sources of information for what to do next. They were like X-ray images that indicated the location and extent of a patient’s disease. The answer is not to digitally alter the images to make it look like the disease is gone, but to allow the patient and his doctor to go through the healing process with accurate information.

In short, the Federal Reserve prevented the whole economy from going through the healthy correction they needed since the last Fed-induced boom-bust cycle.

The Importance of Market Interest Rates

Ludwig von Mises, the great Austrian economist, was the first to put forward the theory on how central banks cause the “boom and bust” business cycle. It’s based on the fact that businesses rely on market interest rates to make sustainable choices about what projects to pursue and also how many people to hire and what sort of capital goods are needed to pursue those projects.

Without interference from a central bank, the interest rate performs a vital balancing act between borrowers and lenders. Their interactions, which reflect their value judgments concerning the economy’s saved resources, cause interest rates to rise and fall.

Without interference from a central bank, the interest rate performs a vital balancing act between borrowers and lenders.

For example, if people begin to save more and are ready to lend their extra savings to potential borrowers, the interest rate falls for the same reason the price of bananas would fall if a bumper crop of bananas flooded the market with the yellow fruit. The stock of saved resources (land, building materials, equipment, etc.) is shifted over into the hands of borrowers, who will use them for their desired purposes, including expanding their businesses, buying homes, or even starting a new business.

In the cases where somebody borrows to expand or start a business, they will only do so if they expect to earn enough money to pay back what they borrowed plus interest and hopefully have some profit left over for themselves. The interest rate, therefore, not only performs a balancing act but also serves as a standard for entrepreneurs to judge which business projects are worth pursuing and which ones aren’t.

Central Bank Interference

This process of efficiently allocating saved resources to the best and most productive uses, based on reliable and precise information from credit markets, turns into a jumbled mess when central banks interfere.

When the Fed artificially expands credit, it pushes interest rates down and makes it look like there is a larger stock of saved resources than there really is. Businesses take the new funds to hire new workers and purchase new factories, tools, machines, and all other kinds of capital goods. At the same time, consumers also take advantage of the cheap borrowing to purchase homes, cars, and all other kinds of consumption goods.

When the Fed artificially expands credit, it pushes interest rates down and makes it look like there is a larger stock of saved resources than there really is. Everything looks great. Employment goes up as businesses expand hiring. Incomes go up as people find new jobs. Businesses see their inventories fly off the shelves during the spending binge. Stock prices respond, perhaps reaching new highs as investors look at the businesses’ earnings. Amateur investors also find it easier to buy into the market because their own incomes are up and it’s difficult to make the wrong picks when everything is doing well.

The Consequences of Easy Money

Has the Fed created prosperity for nothing? Can we just run the money and credit spigot endlessly with no real consequences?

Unfortunately not.

New green pieces of paper or entries in accounts do not increase our productive capacity. New loans and credit cards with low interest rates don’t either. In fact, underneath the surface of happiness and optimism, we were actually destroying our productive capacity. We were consuming our resources and failing to maintain our capital goods.

The artificially cheap credit disguised the real availability of capital. Also, the projects pursued by businesses weren’t the right ones. They were tricked into pursuing riskier projects with a longer time to completion due to the false information from credit markets.

The artificially cheap credit disguised the real availability of capital. It looked like we could do projects A, B, and C when we really only had enough resources for A. The prices of the increasingly scarce capital goods begin to rise above what anybody expected. Even though we are halfway finished with projects B and C, we realize they can’t be finished, so we abandon them and all of the workers employed in those projects have to find a new job.

The Bust Is a Healthy Correction

The bust begins when the money spigot is turned off or slowed enough for people to reconsider how they have allocated capital in light of new expectations about future interest rates and the profitability of their current projects. (Predicting the exact timing of the bust is difficult, because so much of the economic data has been falsified and because it is dependent on everybody’s perceptions and expectations.)

The bust must be allowed to take its course. The bust, even though it is marked by rising unemployment, falling stock prices, and bankrupt businesses, is actually a healthy process. The bust must be allowed to take its course so that we can readjust who is doing what job using what tools based on the real availability of saved resources.

By reinflating, we only kick the can down the road and make for ourselves an even bigger problem. We can prop up stock prices and paper over our fundamental problems, but we cannot fix one business cycle by causing another one.

Conclusion

Is the stock market indicating that we are on our way to another bust? Will we finally go through the healthy correction we need to have a stable, sustainably growing economy? These are questions we cannot answer with certainty today.

What we can say with certainty is that the decade-long rally in stock prices cannot be based on a new era of sustainable growth and productivity. In fact, the stock market indices have grown just as much as the Federal Reserve has inflated, and this is borne out by multiple measures of both.

We would expect the stock market to reach new highs after unprecedented expansionary monetary policy. Business and employment should look great after a few years of near-zero interest rates and easy money.

But we also shouldn’t be surprised when the inevitable bust follows the boom.