Privatize Social Security and the economy will roar back

It is always a good time to privatize Social Security. In the long run, it is better for people to save for retirement, via portfolios of stocks and bonds, than to be dependent in old age on government handouts. The long-run case for Social Security privatization has been discussed before, especially in 2005, when George W. Bush had just been elected on a platform featuring Social Security reform. But doing it now has short-run benefits. Privatizing Social Security is the best way to get us out of this economic slump. Here’s why.

In broad terms, a pay-as-you-go system of public pensions, such as America’s Social Security program, reduces the overall savings rate and therefore the growth of the capital stock and the economy. It corrupts the political system, turning it into a tug-of-war for society’s resources, as older generations demand payback for years of forced contributions, but get it from younger generations’ current production, via public tax-and-transfer systems. The government gets more current income, which it spends, and long-term obligations, burdening future taxpayers. Pay-as-you-go systems cheat the future, but the government can’t save without partially nationalizing private banks and corporations.

As for the current recession, economists and other pundits have a number of explanations. Keynesians like Paul Krugman and Matt Yglesias blame a “liquidity trap,” in which further injections of liquidity don’t stimulate the economy; they just get hoarded. In their own way, “market monetarists” like Scott Sumner (who blogs at www.themoneyillusion.com) believe this as well.

On the other side, Tyler Cowen sees the 2008 financial crisis and the slump that followed as a symptom of a “Great Stagnation” that has been decades in the making, while Casey Mulligan argues that we are suffering a “redistribution recession” because minimum wages, more generous unemployment insurance, and other policy changes have made people less willing to work.

Escaping the Liquidity Trap

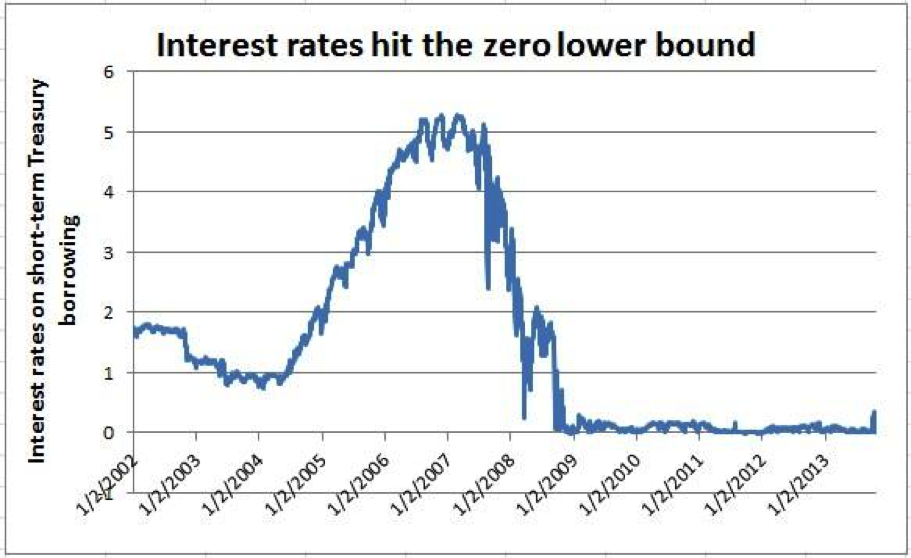

All of them are right. But it is the liquidity trap that Social Security privatization could solve. Two charts will help to illustrate what the liquidity trap means. First, look at business investment (using Bureau of Economic Analysis data):

Whereas strong business investment created jobs and raised wages during the late 1990s boom, business investment grew slowly under Bush and plummeted under Obama. I constructed a somewhat arbitrary but nonetheless revealing “trend” based on the years 1967–1996. By this standard, business investment is about 14 percent too low. Second, look at the time path of the “safe” interest rate paid on U.S. Treasury bonds:

Do you see what’s happening? Since 2008, interest rates have stopped their normal fluctuations and become stuck at the zero lower bound. That’s the liquidity trap.

The obvious part of the liquidity trap is that U.S. Treasury bonds can’t pay less than 0 percent nominal interest. If they did, investors would hold cash instead. The subtle part is that just because interest rates are stuck at zero doesn’t mean the forces that affect the interest rate have stopped operating. Rather, it is a safe bet that the natural equilibrium interest rate has been fluctuating as usual, only in negative territory. Money, by offering a riskless 0 percent return, has been preventing the market for investment funds from clearing properly.

The Natural Interest Rate

The natural rate of interest is a tricky concept to understand. Start here: Economic growth requires risk-taking. Indeed, even for the economy to hold steady requires risk-taking, since even routine maintenance is an investment that may not pay off. But initiating new economic activity—launching new projects, developing new products, building new plants, founding new companies, hiring new employees—usually involves more risk. To attract investors to a risky project, you need to compensate them. You need to offer a risk premium.

In an investments class, you might be taught to treat the rate paid on T-bills, or the “safe” interest rate, as a baseline to which a risk premium must be added to attract money into riskier asset classes. To understand the concept of the natural or equilibrium interest rate, we can turn this around. Think of the expected rate of return on the risky projects entrepreneurs want to pursue. Then subtract the risk premium. That’s the natural rate of interest.

Of course, that explanation is a bit vague and oversimplified. Entrepreneurs have many projects in mind; not all will be pursued. There are many different risk premiums, and financial markets cunningly sift through it all in setting asset prices that balance risk and return. Still, for present purposes all we need to understand is that the natural rate can be negative, if entrepreneurs’ projects offer rather poor returns and/or investors are especially risk-averse.

That is what has happened since 2008. Why is debatable. If we believe in Cowen’s Great Stagnation, we might say there just aren’t many good projects around for entrepreneurs to pursue right now. If we believe in Mulligan’s redistribution recession, we might say that unemployment benefits are turning potential entrepreneurs into couch potatoes. Uncertainty, especially due to huge deficits and Obamacare, is a major culprit in the eyes of the business community, but uncertainty is hard to measure. Keynesians like to say investment is down because aggregate demand is down: Why build capacity when you have too much already? That can’t be the whole story, because much investment is oriented toward the medium- to long-run future. The graying of the U.S. population may be reducing investors’ collective appetite for risk. Seniors, set in their ways, like fixed incomes. Whatever the reason, interest rates don’t lie. Expected returns on entrepreneurs’ projects, minus risk premiums, must be zero or less. Otherwise, investors wouldn’t buy T-bills that pay so little interest.

When interest rates hit the zero lower bound, you’re in a liquidity trap.

The Money Store

Money is said to have three functions: (1) as a medium of exchange, (2) as a unit of account, and (3) as a store of value. In normal times it is a poor store of value. When you get it, you want to either spend it or buy assets that pay interest. At the zero lower bound, though, money becomes competitive as a store of value.

This can initiate a vicious cycle. With interest rates at zero, people start taking cash out of circulation to use it as a savings vehicle. Money in circulation gets scarcer and rises in value vis-a-vis goods—that is, prices fall. Deflation makes the real return on holding money positive: Hoard a dollar today, and it will buy more tomorrow. So hoarding leads to falling prices, which encourages more hoarding. That’s more or less what happened in the Great Depression.

The Fed since 2008 has been determined not to let that happen again. It flooded the system with money and, though housing prices fell sharply, it prevented a general deflation. But we’re still stuck at the zero lower bound.

In a liquidity trap, entrepreneurs who could use investors’ money to grow the economy have to compete for investment capital against cash and against T-bills that are now almost equivalent to cash. Entrepreneurs would try to create real future value. Cash and T-bills don’t. So when money goes to cash and T-bills instead of to entrepreneurs, too little economic activity occurs. But we can’t get out of the liquidity trap by abolishing cash. So what is to be done?

We tried fiscal “stimulus” in 2009. In the wake of the financial crisis of 2008, federal deficits surged to over $1 trillion per year. In Keynesian theory, tax cuts and extra spending should have boosted consumption by putting more money in people’s pockets, but they didn’t. Instead, people and firms saved more. That’s just what “Ricardian equivalence,” the theory that people are rational and save to offset future fiscal policy, predicts.

Since 2011, the government has raised taxes and begun to bring spending under control. In Keynesian theory, these moves should have curtailed consumption, but they didn’t. As the government began to get the budget under control, the stock market surged. Consumers with less disposable income but more wealth have little reason to cut their spending. Again, the facts fit “Ricardian equivalence”—a nemesis of Keynesianism—operating in this case via stock prices.

Although the Fed’s normal methods for managing the macroeconomy via interest rates don’t work in a liquidity trap (if they ever do, which is debatable), the Fed could get us out of the liquidity trap by printing enough money to ignite inflation. In that case, since cash would be losing value, entrepreneurs’ projects would become relatively more attractive to investors. But inflation makes it hard for people and firms to make long-term plans. Relative prices become maladjusted, as some rise faster than others, causing inefficiency. A lot of unfair redistribution takes place: for example, from lenders to debtors, or from people on fixed incomes to landowners and workers. Once inflation gets started, it’s hard to control. That cure may be worse than the disease.

A Way Out

So far, so bleak. And yet there is a solution. The irony is that even as investors’ high demand for government debt is causing all these problems for the economy, there is a lot of quasi-government debt outstanding whose owners would be happy to sell it, if only they were allowed to do so. This debt consists of the Social Security Administration’s largely unfunded promises to future retirees.

Legally, these promises are not debts. According to the Supreme Court decision Flemming v. Nestor, there is no right to collect Social Security benefits; Congress can revoke them at will. It would be nice to convert these revocable “entitlements” into real property rights, but how to do so is tricky.

Transitional challenges aside, Social Security privatization would essentially convert people’s entitlements to future Social Security benefits into explicit government debts contained in private accounts. That done, individuals would be allowed to sell at least some of these bonds in exchange for private-sector stocks and bonds—and they would, since stocks perform best over the long run, yielding an average of 7 percent per year. Volatility doesn’t matter for workers far from retirement. So Social Security privatization would lead to (a) a flood of Treasury bonds into the bond market, and (b) a flood of money into the stock market, as individuals optimized their portfolios.

With so many new Treasury bonds coming into the market, flight-to-safety investors would be more than satiated. The government’s liabilities under Social Security are huge, and there’s no way investors would buy them all at a near-zero interest rate. Interest rates would rise. We would be free of the liquidity trap.

At the same time, the new money flowing into the stock market would push stock prices up further, and that would drive a revival in business investment. Nobel laureate James Tobin long since explained why high stock prices promote business investment, and the data back him up. Stock prices express the market’s opinion about what the existing capital stock is worth, and therefore whether it’s worth making more of it. When stock prices are low, the best way to get structures and equipment is to buy existing firms that have them, not to build. When stock prices are high, entrepreneurs are motivated to start new companies and make initial public offerings. Existing companies can sell new shares to raise capital to finance new ventures.

As Social Security privatization raised stock prices, therefore, it would fuel a boom in business investment, leading to job creation and rising wages. Goodbye, economic slump. The financial logic is a little tricky, but here’s the essential point: Someone needs to take risks to get the economy moving, and Social Security privatization would empower ordinary Americans to do it.

Social Security privatization is more a smart-government reform than a small-government reform, though it does give individuals a bit more say in how their lives are run. It has been adopted both in the world’s best-run capitalist mecca, Singapore, and in the world’s best-run social-democratic welfare state, Sweden.

Ironically, especially for a free-market economist like myself, Karl Marx provides some inspiration. Marx wanted the workers to own the means of production; Social Security privatization would bring this about. Through private retirement accounts, ordinary workers would own shares in the private firms that own the country’s productive capital stock. That promotes social solidarity. Workers of the world could unite—to make bets on the country’s future. With that vote of confidence from all these newly minted capitalists, the economy would come roaring back.